During our participation in the latest edition of DCAT in New York, one of the recurring topics of debate with our partners and clients revolved around the current state of the generic product market, where the general consensus was that one of the biggest current challenges for the generic drug industry lies in increasingly intense competition, with consequent erosion of margins.

In this article, we will examine the evolution, prospects, and current challenges of the generic drug market in the United States and ultimately explore whether this is an absolute truth or offers nuances.

Evolution of the generic drug market in the United States

The Office of Generic Drugs (OGD) of the United States Food and Drug Administration (FDA) has been instrumental in the growth of the generic drug market in the United States. Since the passage of the Drug Amendments Act of 1984 (Hatch-Waxman), OGD has established a generic drug review and approval process that has expedited the introduction of new products to market. Since 1984, the OGD has approved more than 32,000 generic drug applications, giving patients access to quality drugs at a much lower cost than brand name drugs.

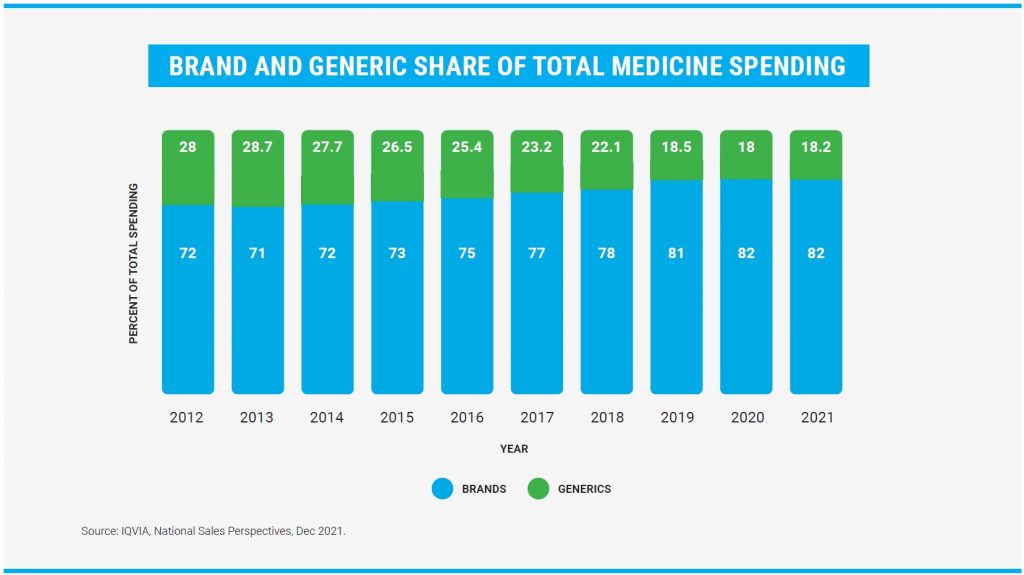

In recent years, the generic drug market has experienced steady growth in the United States. In 2022, more than 1.6 billion generic drug prescriptions were sold in the United States, representing more than 91% of all prescriptions. However, they only account for 18.2% of total drug spending in the United States. According to the OGD annual report, a total of 914 generic drugs were approved in 2022 (742 approvals and 194 provisional approvals), and from 2015 to 2022, more than 7,000 generic drugs have been approved in the United States.

Prospects and Challenges of the generic drug market in the United States

Although the US generic drug market has experienced steady growth in recent years, there are some unknowns about its future. And one of the main challenges in the generic market is competition.

According to data from the Generic Pharmaceutical Association (GPhA), there has been a significant increase in the number of generic drug manufacturers in the United States in recent years, from 72 in 2010 to more than 130 in 2020. This increased competition has led to an increment in price pressure and has forced generic manufacturers to seek new strategies to differentiate themselves from the competition and maintain their profitability.

In the United States, generic drug prices have fallen steadily in recent years, in fact generic prices are now at their lowest level since 2009. According to a report by the GPhA, prices for generic drugs in the US decreased by an average of 9.3% in 2019 compared to the previous year.

In general, generics are launched at much lower prices than the original or reference product. According to the same GPhA report, in 2019 the average price of generic drugs was $0.93 per unit, compared to the average price of $155.22 per unit for brand name drugs. This price difference is due in large part to the fact that generic manufacturers do not have to incur the same research and development costs as brand name drug manufacturers.

Another major challenge is the increasing regulatory pressure and the complexity of the FDA’s approval processes. Although the FDA has tried to streamline the generic approval process, it can still take years for a generic product to gain approval and enter the market. In addition, the FDA has also increased its quality and safety requirements for generics, which may result in additional costs for manufacturers of these types of products.

When it comes to the specific challenges by dosage form, there are some notable differences. For example, injectable generic drugs are generally more difficult to manufacture and may have a higher failure rate for FDA approval. According to a report by consultancy IQVIA, in 2020 only 30% of injectable generic drugs submitted for FDA approval were approved, compared to 75% of oral generic drugs.

Finally, generic drugs face unique challenges in terms of acceptance by physicians and patients. Often doctors and patients are more familiar with brand name drugs and may have reservations about switching to a generic drug. Generic drug manufacturers must work to educate doctors and patients about the safety and efficacy of generic drugs and address any resistance they may encounter.

What about transdermals?

We have seen the US generic drug market experience significant growth in recent decades. However, and due to the inexorable logic of the market, the scenario has become more competitive and complex. The entry of multiple competitors (mainly from India and China) has triggered a price war, as we saw above, which, added to the increasing regulatory complexity, results in a less attractiveness of this segment of generic medicines.

However, this is not a scenario applicable to all pharmaceutical forms, there are meager niches within the universe of generic products that present different realities. We mentioned at the beginning of the article that in the period between 2015 and 2022 a total of 7,239 generic products were approved by the FDA, among which only 84 of the total were transdermal patches, which represents only 1.2 %.

When it comes to prices, of course, generic transdermal patches also tend to have lower prices than brand name products. However, according to a study published in the journal American Health & Drug Benefits in 2019, generic transdermal patches are priced 22-48% lower than brand-name products at launch.

Complementing this information, according to a study conducted by the University of Pittsburgh Drug Price Research Group in 2019, generic transdermal patch prices were, on average, 12.3% lower than original patch prices.

In line with the above, a 2018 FDA report indicates that most generic transdermal patches are priced between 50% and 70% of the price of the reference product.

While there is some variability between studies, probably related to various factors (market size, molecule, technical complexity of the product, etc.), we see that generic transdermal patches are more affordable for consumers compared to reference products, but that price drop is negligible when compared to the case of other pharmaceutical forms that represent a relationship of only 2% of the value of the brand product during the first year from the entry of the generics.

Patches: the real state of generic products.

There are several factors that can explain the price difference between generic and originator products in the transdermal patch market. One of the main points is the complexity in the formulation and manufacture of this pharmaceutical form, which requires very specific expertise and know-how. In addition, transdermal patches often require specific technologies and materials to ensure the efficacy and safety of the product, which can also increase the cost of production.

Another important factor is the level of competition in the transdermal patch market. While the number of companies dedicated to developing and manufacturing transdermals has increased, it has done so at a slower pace compared to the companies involved in generic products. Furthermore, the transdermal patch market is relatively niche, which may affect the supply and demand of generic products.

This is evident in the number of generic products available in different pharmaceutical forms. For instance, when we consider the patches with the highest historical sales in the USA and the number of generics available for each of these molecules, we see that there are only limited alternatives, with 7 for Fentanyl, 10 for Estradiol, 8 for Rivastigmine, 3 for Clonidine, 4 for Buprenorphine, and 6 for Scopolamine. This limited number of products and companies offering generics in this segment is in stark contrast to other pharmaceutical forms such as gels, oral tablets, or even injectables, where the options are more numerous.

Within the patch market, some products with reasonable sales of around 30 or 40 million dollars per year have been marketed in the United States for many years, yet they still do not have generic alternatives, as is the case for Selegiline or Methylphenidate.

In general, the price ratio between generic and originator products depends on several factors, including the level of competition, complexity of formulation and manufacturing, and the size of the market. In the case of transdermal patches, the combination of these factors may explain why the prices of generic products tend to be higher compared to other dosage forms.

Returning to the data presented at the beginning of this article, where it is mentioned that the majority of prescription products marketed in the United States belong to the generic segment (91%), a volume that has remained stable in recent years. Combined with the share of total medical spending, which has decreased from 28% to 18.2% in the last ten years, it is clear that this market has passed its maturity stage, where it reached its maximum volume of sales, but with a clear pressure on costs exacerbated by strong international competition.

For most companies in the pharmaceutical industry that have multiple forms of administration within their product offerings and that analyze the generic market comprehensively, they probably do not find great attractiveness in this segment and prefer to evaluate opportunities in other segments, such as the growing popularity of 505 (b) 2. However, for those of us who are exclusively in this niche and analyze the segmented variables in-depth, the generic market is truly attractive. Only 30 patches have managed to reach the US market, with a limited number of generics, as we have seen, which, in turn, have had a much lower price drop than what has occurred in other pharmaceutical forms.

If we add to these factors that it is a niche with high entry barriers due to the specific know-how and the particular equipment required for its manufacture, the stability of these products seems to go against the global analysis and what the market perceives.